Variance Analysis Table

I want to analyze project variances...

What is it?

The concept of variances was introduced in the discussion of the budget monitoring report. A variance represents a difference between what was estimated in the budget and what has actually been spent or received during the implementation of the project.

It is important to acknowledge that a budget is an estimate, a projection of what expenditure or income will be during project implementation. Like any estimate, it will not be 100% accurate. As a result, it should come as no surprise that during the implementation phase of the project, actual income and expenses will vary from what was estimated in the budget.

The challenge for project team members is developing the skills needed to analyze why a project variance has occurred, and deciding whether the variance requires follow up actions.

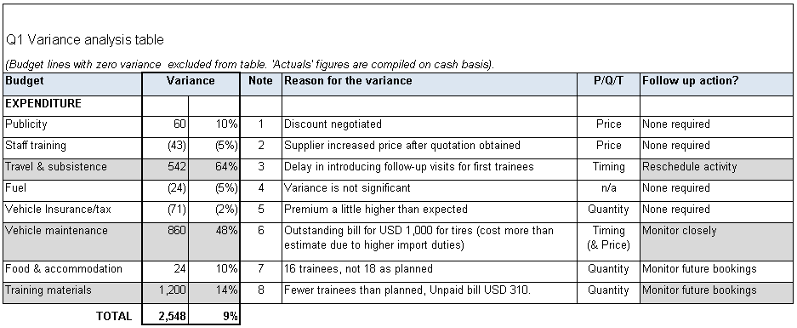

This is the where the variance analysis table can help. The table lists all of the line items in the budget monitoring report that show a variance. The team analyzes the cause of each one, asking “Is the variance significant, what was the reason behind it, and is a follow up action required?”

Because a budget is an estimate of what is expected for project income and expenditure (over specified period), variances will always occur, and this should not be a surprise. It is important to look at the size of the variance, to decide if it is significant or not. A variance of plus or minus 10% is generally agreed to be reasonable. Anything over 10% is considered a significant variance. Negative variances are usually more of a concern, but not always!

How do I use it?

The following scenario from UNITAS describes how the variance analysis table is used in its Capacity Building Project.

The UNITAS team identifies all of the variances in the June budget monitoring report and lists them in a variance analysis table.

As they review the table, they highlight each of the line items with significant variances (they use 10% as a guide to identify significant variances). One of budget lines for Project Materials has a significant variance– this line is underspent by 48%.

Now the project team needs to answer four questions:

- What is the reason for the variance? The project team failed to recruit the target number of garden groups so activities have not been conducted at the level that was planned.

- Is this variance a result of a change in price, timing or quantity? It appears that this is a quantity variance, they don’t have the expected number of groups in place so they have undertaken fewer activities than planned.

- Is this a temporary variance or a permanent variance?

- Temporary variances – variances caused by changes in the planned timing of an activity (eg due to delays or rescheduling) are usually temporary variances, because they will most likely work themselves out during the course of the year. These should be monitored and managed internally, but are generally less of a concern.

- Permanent variances – variances caused by changes in the price or quantity of budgeted items are permanent variances. Once they have occurred, they cannot be corrected and the spending or income will not recover without some action. The only solution is to decide on follow up actions to get overall spending or income back in line with plan. This might be reducing spending on future items where lines are overspent or increase activity levels where savings have been made. Permanent variances are generally more serious and management attention and corrective action is needed. UNITAS’ example is a permanent variance because the planned quantity of garden group activities has not been achieved so far. If they can establish a plan to recruit more groups, and therefore increase the quantity of activities with the groups, then the variance can be recovered and spending will get back on track. - Are follow up actions required? Yes, this is a serious issue. If a plan is not agreed to take some action (eg recruit more groups), the variance will remain, and this budget line will remain underspent all year as activities are below levels planned in the budget. The project could lose funding as it is not spending at the level in the budget, and it may fail to deliver on its objectives.

When do I use it?

To keep on top of the financial management of a project, it is helpful to look at variances on a regular basis, and a monthly review is recommended. Set aside time for this in advance to ensure that all implementing project staff can be involved in the process.

Who is involved?

The budget holder or Project Manager is accountable for management of project finances, and for taking decisions about how to deal with variances. However, the project team must be involved as they are in the best place to help understand the variances and identify appropriate actions for variances.

There will be occasions when issues related to variances need to be escalated to a higher level in the organization in order to be addressed. For example, grant management staff may need to liaise with the funder if permanent variances mean a revision to the budget is required.

Tips:

Sometimes a variance can be due to an accounting error, such as a transaction charged to the wrong account code. So, it’s important to check the detailed transactions and correct any errors found before completing your analysis.

If a variance requires a follow up action, it can be documented in more detail in the Budget Monitoring Action Planner.

Supported & Developed by:

Shared by:

Users are free to copy/redistribute and adapt/transform

for non-commercial purposes.

© 2022 All rights reserved.