Budget Monitoring Action Planner

I want to identify corrective actions for variances...

What is it?

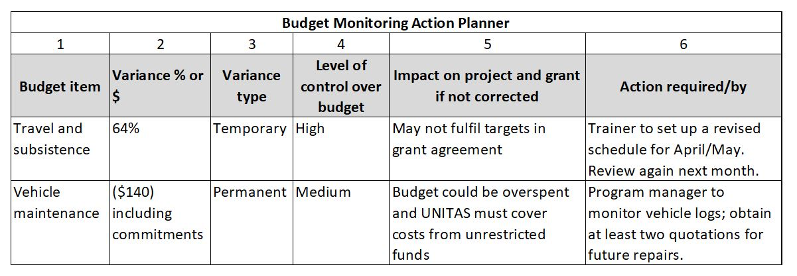

Significant variances identified in the budget monitoring report usually require corrective action. These actions should be documented in the budget monitoring action planner, sometimes called the budget management action planner. The action planner is a table that includes detailed analysis of the significant variances and information about the actions to be taken for each. The information shown in the columns of the planner are:

- Budget item – the account code or budget line description of the type of expense or income, eg. travel and subsistence, vehicle maintenance, venue hire, training fees.

- Variance (% or $) – the percentage or monetary value of the significant variance. The number is shown as a positive (where expenditure less than budget or income over budget) or negative (where expenditure is over budget or income is less than budget).

- Variance type – this column indicates whether the variance is permanent or temporary. Remember that temporary variances will work their way through the system over time, but larger ones might still have an impact on cash flow or activity targets. Temporary variances still need to be monitored.

- Level of control over budget – this column shows to what extent the budget holder has control over this budget and its variance (low, medium or high). For example does the team have the authority or power to make savings if the budget is overspent, or stimulate its use if it is under-spent?

- Impact on project and grant if not corrected – if the variance is not addressed, will there be an impact on the project or the overall grant. For example might this weaken the cash flow, will delays impact on the team achieving project targets, and are variances exceeding allowable tolerances from the funder?

- Action required by – the team should show what will be done and who is responsible, to minimize the impact of the variance and get the project back on track. It is important to note what actions are needed to meet funder requirements, for example undertaking a budget revision, advising funder of delays or requesting a ‘no-cost’ extension. Other actions might involve requesting unrestricted funds to cover over-spends, changing activity plans or making efforts to reduce costs or stimulate spending.

How do I use it?

Use the budget monitoring action planner to discuss and develop agreed actions with your team. This should then be shared with your line manager, Program Manager or the project funder if relevant. Deciding on which actions to take will depend on many factors including:

- Knowledge of the project – how is project progress now and what are the activity plans for the next period?

- Awareness of external factors – what are the trends in inflation? Is the project’s progress or ability to meet targets, dependent on other projects or programs?

- Internal policies – what policies exist related to budgetary control and budget flexibility (or tolerances)?

- Funder rules – consider the guidance from the funder on budget variances and their flexibility on over- or underspending budget lines.

- Significance of the variance – how large is it and how urgently does it need to be resolved?

- Extent of control – how controllable are the budget lines which show a variance?

- Impact – what will be the potential impact if we take no action?

- Availability of unrestricted funds – are funds available that can be used to cover overspending or underachievement of income targets?

Amira is the Project Manager for the UNITAS Capacity Building Project. When reviewing her budget monitoring report she identifies several significant variances which need to be addressed. The project is significantly underspent on Travel and Subsistence expenses and has significantly overspent on Vehicle Maintenance expenses.

For both of the variances, the team discusses the variances and analyzes whether they are temporary or permanent. They answer the following questions:

- What level of control do we have over the issue?

- What is the impact if we fail to correct the variance?

- What actions are required to get things back on track? Who will be responsible for these actions?

When do I use it?

Budget monitoring and reporting is an ongoing process and it’s important to monitor spending on a regular basis, at least quarterly and ideally monthly. Each time you review budget monitoring reports you should develop an action planner to show how the project will deal with significant variances.

Who is involved?

The budget holder or Project Manager is accountable for ensuring regular budget monitoring and for developing action plans to deal with variance issues. This process should involve project team members who bring knowledge of different areas of work and who may be accountable for taking forward a solution.

The budget monitoring action planner supports the quarterly or monthly budget monitoring report. There may also be times when it may be important to share the action plan with the funder of the project, especially if their consent is required to move forward on a follow up action.

Tips:

The budget monitoring action planner focuses on larger variances and permanent variances tend to be seen as more important. However don’t ignore smaller and temporary variances because they can cause cash flow problems and may be an early warning sign of project delays.

It is important that the Project Manager follows up to ensure that agreed actions are implemented.

Supported & Developed by:

Shared by:

Users are free to copy/redistribute and adapt/transform

for non-commercial purposes.

© 2022 All rights reserved.